|

Segregated Fund

|

Mutual Funds

|

Overview

|

Your net premiums are invested in the segregated fund of an insurer which, in turn, invests in stocks, bonds and money market investments. Segregated Funds are insurance products.

|

Money is pooled and invested on behalf of unit holders in stocks, bonds and money market investments.

|

Regulated By

|

Provincial Life Insurance Acts

|

Securities Legislation

|

Investment Growth Potential

|

Yes

|

Yes

|

Investment Diversification

|

Yes

|

Yes

|

Financial Protection

|

At death and maturity, premiums minus withdrawals prorated are usually guaranteed between 75% and 100%

|

There are no guarantees on investment performance.

No limit on potential loss.

|

Death Benefit

|

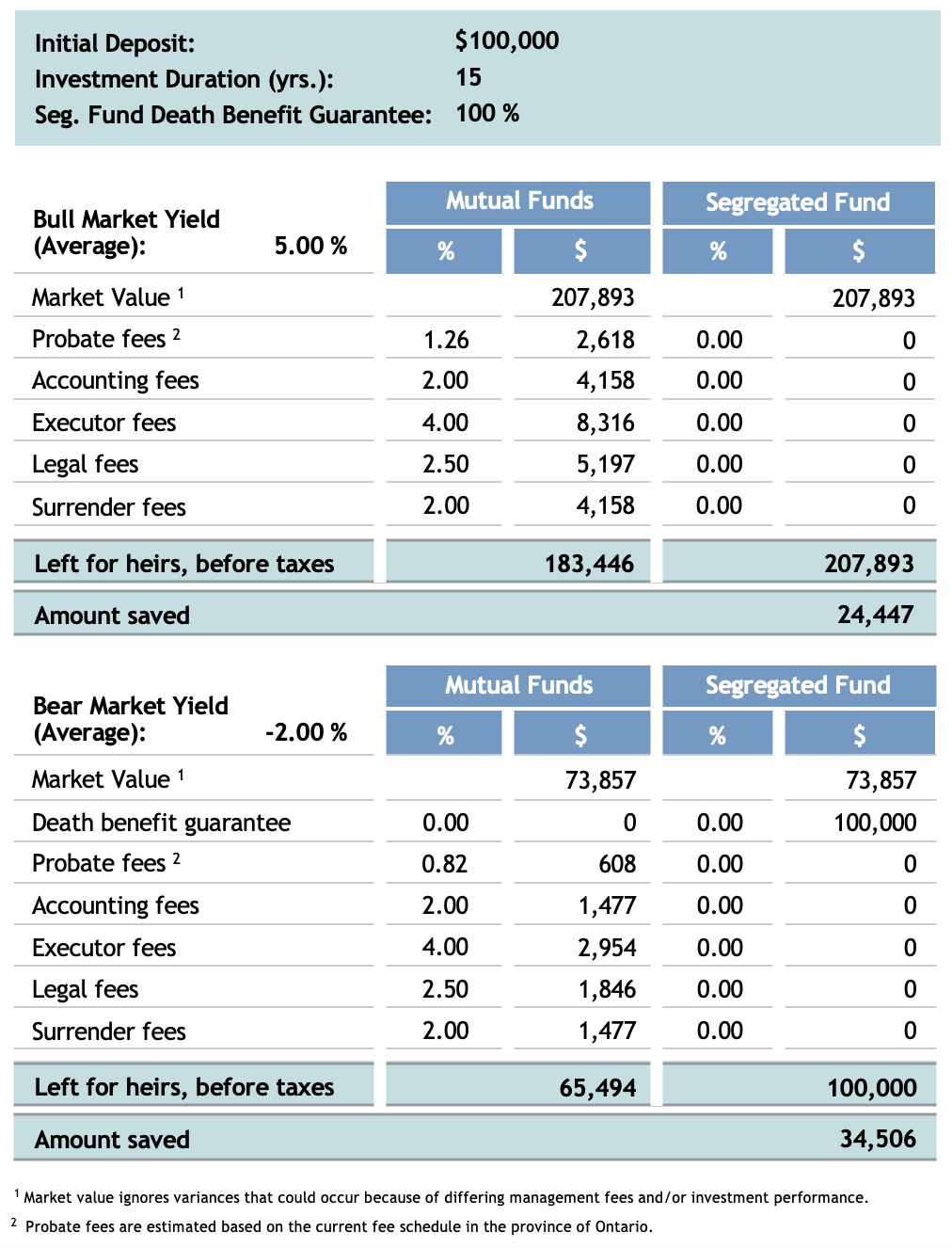

The named beneficiary will receive the greater of, either the guaranteed death benefit or the market value of the policy.

|

The estate or beneficiary will receive the market value of the mutual fund. There are no guaranteed minimums.

|

Probate Protection

|

At death, the named beneficiary will receive proceeds avoiding the estate administrative process and the cost of probate.

|

At death, proceeds are an asset of the estate and are subject to the estate administrative process and legal fees. It may take some time for the estate to distribute the funds.

|

Creditor Protection

|

Designation in favour of a spouse, parent, child or grandchild may result in moneys being exempt from seizure. This is referred to as “creditor protection”

|

No. Assets are open to claims from creditors.

|

RRSP/RRIF Eligible

|

Yes

|

Yes

|

TFSA Eligible

|

Yes

|

Yes

|

Taxation Implications for Non-Registered Investments

|

You are only taxed on the income you actually receive. Taxation is based on how long you own the Segregated Fund units within the income period.

e.g. if you buy units one day before the fixed date, you are only assessed for the one day’s income.

You can use the capital losses to offset the capital gains from other sources.

For accounting purposes, acquisition fees are excluded from the Adjusted Cost Base (ACB) and treated separately.

|

There is the potential to be taxed on income never received. Taxation is based on who owns the mutual fund units on a given date at the end of the income period.

e.g. if you buy units one day before the end date, you are assessed for all income earned in that period, even though you did not benefit from that income.

Capital losses must be carried forward and are not allocated to you, the unit holders.

Acquisition fees are included in the Adjusted Cost Base (ACB).

|

Under what circumstances might these be more suitable?

|

Non-Registered and Registered Funds. Investors approaching or in retirement.

Investors who are more risk averse and prefer security and guarantees.

Business Owners who want creditor protection.

|

Non-Registered and Registered Funds.

Investors who want a wide variety of specialized funds.

Investors who are willing to give up guarantees for potential increased returns.

|