So many options when it comes to Life Insurance and Insurances… How do you know what to choose? Life insurance comes in many shapes and sizes and finding the right fit for your life can be daunting to say the least. It can be tempting to simply find the least expensive solution and go with that. But like all products, sometimes the least expensive option can end up costing you more in the long run.

Here is a break-down of what kinds of options are out there.

Life Insurance (Term, Whole Life, Universal Life)

Term Insurance

Term Insurance Is insurance that you use for coverage for a period of time. Term Insurance is the low-cost option. This product provides you with a set death benefit for a set amount of time (10 years, 20 years, etc.). When that time’s up, your coverage is renewed at a higher cost if you don’t cancel your coverage. You can also convert it to a permanent life insurance policy without having to answer questions about your health.

Term Insurance with its lower initial cost compared to permanent life insurance, is a popular way for those just starting out to protect themselves and their families. Term life insurance is usually less expensive than permanent life insurance, so you may be able to purchase more coverage. You may even want to consider a mix of a little permanent with some term insurance.

Here are some examples of why someone might get a Term Insurance policy. When someone gets a term policy, they want that insurance for the term selected. A parent might get a term policy that covers their children while they would need more coverage, probably up to age 20 or so, by then their children should be okay on their own if something were to happen to you as they are no longer dependants. Another example of why someone would purchase Term Insurance is for the term of their mortgage (see below for the difference between Mortgage Insurance from the bank and Term Life Insurance).

Whole Life Insurance

Insurance that lasts from now until the day you pass away is called permanent insurance, and it comes in many different forms. One of the oldest and most successful is called Whole Life. You can likely guess why it’s called that (because it covers you for your Whole Life).

Whole life policies are considerably more expensive than your typical term policy. Generally, there are two ideal use cases for a whole life policy. The first is to maximize the estate that you leave your loved ones. Participating Whole life policies tend to return very favourable rates of return over time, and the death benefit is received by your beneficiaries tax-free, resulting in a very effective way of building a legacy for the next generation.

The other case is for building up value to be used during your life. By using a form of the product that builds early cash values, you’re able to borrow against the value in your policy to fund education, retirement, or any other lifetime need. When you pass away your tax-free death benefit can be used to repay any remaining debt.

Universal Life Insurance

Like Whole Life, Universal life insurance is permanent, meaning it lasts the rest of your life – as long as you pay the premiums. Universal life insurance combines the advantages of a permanent, lifelong policy with a tax-advantaged investment component.

So, what may make universal life insurance right for you? The short answer: flexibility. This kind of insurance typically lets you select your preferred premium schedule, the amount you want to pay (within limits) and an investment mix that matches your unique risk profile.

Living Benefits (Critical Illness, Disability, Long Term Care)

Critical Illness

Critical illness can give you a tax-free payment if you’re diagnosed with a serious condition. Your contract will define which conditions you’re covered for, but some examples include cancer, heart attack or stroke.

Coping financially with an illness is just part of the picture. Having access to emotional support and medical treatments can help your recovery.

Reasons why you might want to consider having Critical Illness Insurance, are that firstly, it’s more common than you think; A serious, life-altering illness affects one in three Canadians in their lifetime. Secondly, it covers daily costs – you can use your payout to help with your expenses while you recover. You also protect your retirement savings and other investments, which you won’t need to dip in to pay for additional medical costs. Lastly, you get to focus on your recovery, concentrating on getting healthy knowing that your benefit payment will help you with your finances.

Disability insurance works when you can’t. It can give you tax-free monthly income to help pay expenses if an illness or accident stops you from working.

While a disability can often be visible to the naked eye, not all disabilities are so easily recognized. Chronic pain or a mental health issue can also qualify as a disability.

Reasons why you might want to consider having Disability Insurance, are that firstly, it’s very common to become disabled – up to 40% of Canadians become disabled for 90 days or longer before age 65. Disability Insurance will replace most of your paycheque – Potentially receive up to 80-90% of your take-home pay. And Lastly, you protect your retirement savings since Disability insurance can help you meet your financial obligations so you may be able to avoid dipping into your retirement savings.

Many do not take into consideration the cost of long-term care. The sad fact is is that many people think that the government will look after them and there is no need to worry about anything else because if they get hurt or disabled the government is just going to step in and pay for everything. (NOT TRUE!!) The availability of care that is out there is very minimal and the government is stretched to the limit. So then there are private agencies – which cost money… and the government is not going to pay for this for you, so you will end up having to pay and it is very pricey.

How does long term care work?

Long-Term Care is similar to the disability tax credit – meaning that you have to provide proof that you can not look after yourself. Normally there are 5 activities of daily living to take into account:

Getting out of bed

Transferring position (ex. getting out of a chair and going to another location)

Going to the bathroom

Washing yourself

Dressing and Eating

Those are your 5 activities of daily living and if you can not do 2 out of those 5, whether it’s for a mental reason – whether you have had a stroke, have dementia or alzheimers, or whether it’s for a physical reason – if you slipt and fell and broke a hip or leg, etc. You now have a claim if you can’t do 2 out of the 5.

The doctor or hospital will assign someone to make the assessment that you need care and the level of the care, which includes checking out your house situation. Do you need help getting dressed, preparing meals, washing, getting out of bed, etc. Then they will assign a personal support worker and/or nurse to come in and see you. They will assign them maybe 2 days a week and maybe they will come get you out of bed at 6 am, because that is when they have the time (because the government is stretched so thin), but how do you get out of bed the other 5 days a week? What if you need support every day, what do you do then? Then it’s on your dime. You have to come up with the money to afford this. The best thing is to have your own personal support worker and pay for it yourself so that some one comes when you want and as often as you need.

Having your own Personal Support Worker

Costs money, and if you haven’t looked into Long Term Care Insurance this will be coming out of your investments or savings. This means disrupting your retirement plan or your estate plan in order to get you basic care. People spend years accumulating a nest egg to enjoy in their retirement… and it can be devastated if you need care.

When should one start looking at Long Term Care Insurance?

The best time to think about Long Term Care Insurance is around 55 years of age when you are starting to plan for retirement, it’s another guarantee to your plan. You can, however, get Long Term Care Insurance from age 18 onwards and like any insurance, it is way less expensive and easier to obtain the younger and healthier you are.

Is it easy to get?

It is pretty easy to get unless you are pretty bad health-wise. For example, type 2 diabetics typically qualify for the plan. There is a medical declaration, but no medical questions. It is also pretty affordable.

How the Long Term Care Insurance works

Long Term Care Insurance works like a reimbursable plan. You basically purchase a pot of money and you are provided with levels of coverage. Meal reimbursement… Just keep your receipts! (meals on wheels, ordering pizza, etc), Payments for house adjustments to make it more accessible, payments for crutches, wheelchairs, etc, various medical assistance, and you draw down on this plan till it is done.

It is designed primarily to keep you at home as long as possible, (statistics show you live longer while at home rather than in a long term care facility). It also works as a bridge between home care and the long term care facility. Long Term Care Facilities usually have an average wait of 5 years to get into. You can also attach a rider for an additional cost to your Long Term Care Insurance Policy that will pay for your Long Term Care Facility as well.

Child Insurance

Insurance for Your Children

No one wants to go through the death of a child but for the benefit of the child, everyone should consider child insurance. There are two ways to do it; a child rider or a stand-alone policy, both with their own benefits to consider.

Child Term Rider

Any family that has a child should at the minimum have a Child Rider including each child. It is the cheapest and easiest child insurance, you just add it to a Whole Life or to a Term policy. You can get up to $25,000 (max) per child. Whatever you buy in a rider, it’s each. Typically $10,000 per child is what people get, which typically costs about $3 in premiums total for all the kids per month, each child gets covered for that $3 face amount. Having said that, you do have to provide details of your kids, because not all kids may be covered, since major issue like cerebral palsy is probably not be covered. You will be asked questions like age, height, premature at birth, etc. Every time you have another child you can’t assume they are covered – you must notify the insurance company of the child, with their height, weight, etc. (but it does not change the premium monthly cost for all the children).

The children’s coverage lasts until age 21, maybe to age 25 if they are at home in post-secondary. At age 21 you will be notified by the company that you can exchange/convert the Child Rider with permanent insurance, with no medical where you can get up to 5x what they were initially covered for and that is with no medical guaranteed at the cost of that age (21 years old).

Stand Alone Child Insurance

There are many benefits of a Stand Alone Child Insurance policy. First of all, later on, it ends up being cheaper, you also get limited pay options which you don’t get on a Child Rider, you can have a policy paid up in 20 years, while the policy increases in value over time which is cheaper when getting the policy when one is younger.

You can get a policy with paid-up additions. When you buy an individual policy for your child, it is a Whole Life policy that creates dividends. Dividends are a profit the insurance company makes and then you get a profit which you can purchase more insurance with. Later in life, the child can take that insurance and borrow from their built-up cash values for whatever their needs are, retirement, or a down payment on a home, etc.

So the advantage of going with a stand alone policy is that it’s cheaper, has limited pay options, dividends, can buy more insurance, there is no maximum coverage with this type of policy. Plus you can add a guaranteed insurability benefit rider to your stand alone policy – which means starting at age 21 they will be offered to buy 10 times the face amount with no medical assessments. The offers happen every 3 years, there is an offer of 10,000 and then also included in the 10 is on your first Marriage and your first house (which you have to apply for). Every 3 years is 24, 27, 31, 37, 40, 43. And you will get one more (it’s 10 times). You don’t have to take the offer. If you don’t take the offer it will expire, and you can take the next one (or not).

What happens if I drink or use cannabis? Who is a “smoker” and what does that mean for my premiums?

Cannabis Use

Some people think that you can’t get Life Insurance if you smoke weed or take cannabis products but that’s not the case. Every case is different, some companies won’t insure, while some will, some companies will issue standard rates, some will rate you, and some will flat out deny you. As a brokerage, we can shop around for you and find something fitting. Contact us today to find a plan that will work for you.

Alcohol

Insurance companies will ask if you drink and how often, potentially rate you accordingly, probably alongside any medical conditions and/or family history.

Smoking Cigarettes

Smokers are rated. You simply may not live as long as a non-smoker and you are rated because of this. If you stop smoking for 1-2 years (depending on the company you are insured with) then you can contact your Life Insurance company and they may lower your premiums to that of a non-smoker.

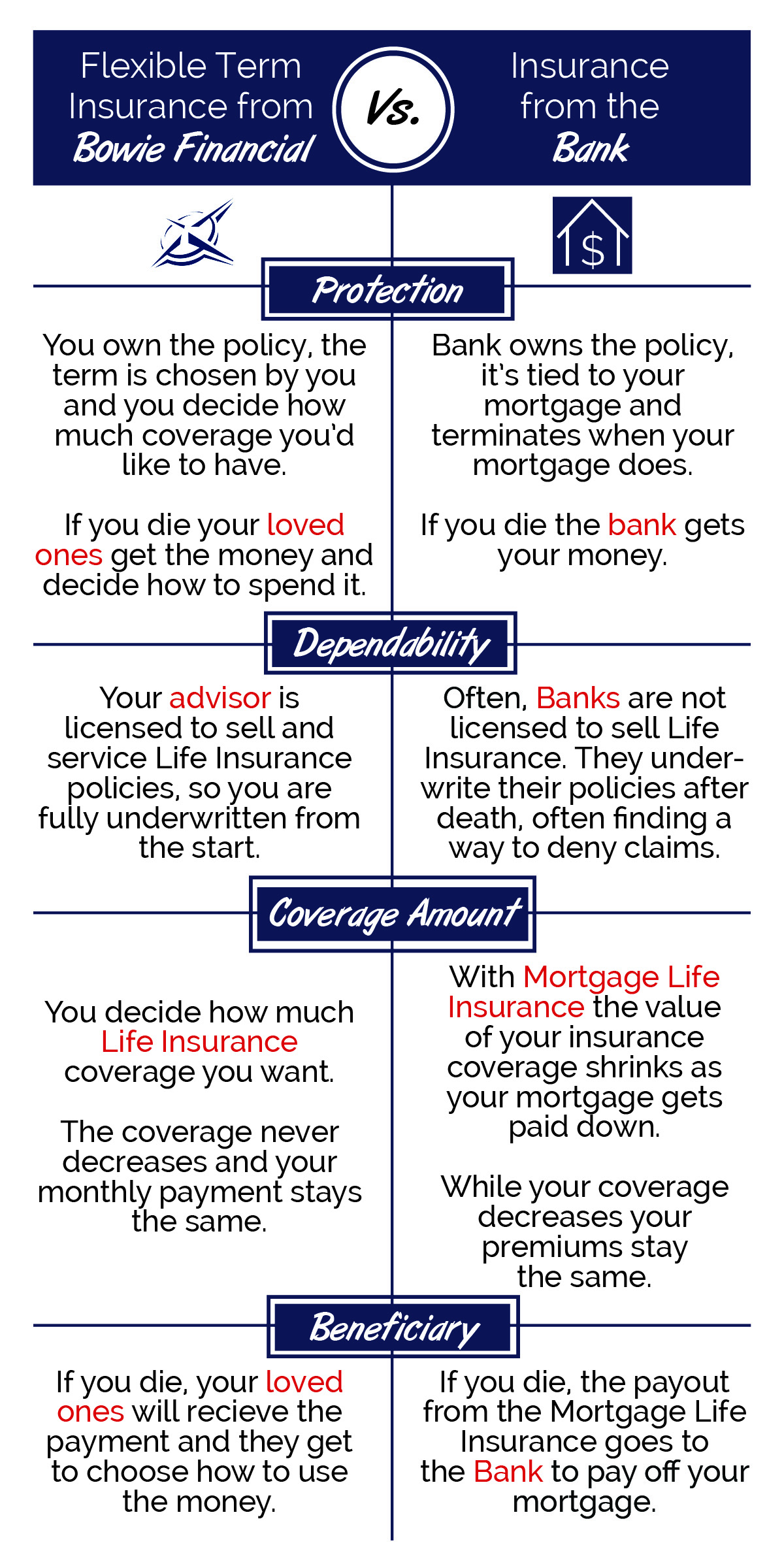

Mortgage Insurance Vs. Term Life Insurance

Do you own a home? If you do you probably have some sort of Mortgage Life Insurance, or maybe you have Term Insurance, or maybe you have both? Do you actually know what you are paying for? You might not. Most people don’t know and that’s okay!

When you get a mortgage at the bank they hand you a package of papers to sign that might be taller than you. Let’s face it… you are so happy and over-joyed you’ve just bought a new home, yay… that you may not realize you just bought Mortgage Life Insurance.

Did you know that Mortgage (Bank) Life Insurance only covers you while you have a mortgage and if you die the bank gets your money (since the bank owns the Policy). It is protection you pay to cover the bank’s interests. It decreases as your mortgage is paid off but your premiums stay the same. So you are just paying to protect the bank, you may get nothing out of this type of coverage because they don’t even do the underwriting when you buy it, so in the chance you die; they will do the underwriting then and could find reasons not to pay out.

Instead, you can re-allocate your money and get more from it!

Did you know that you can replace your Mortgage Life Insurance with Term Life Insurance and you will own the policy, it will probably cost you the same or less, but you own it which is the most important! When you die, your loved ones get the money, (not the bank), and they can do whatever they want with it. For example; they can choose to take the money and pay off the mortgage or they can pay off some higher interest loans, and/or pay for your funeral and estate expenses….whatever they want, whatever is best for THEM.

Check out this chart we created for a quick reference to see the difference between the two types of insurance.